| analytical Q | Suggest a Link | Contact | Search | Energy |

final published PDF in Platts Energy Business and TechnologyHTML version on Platts.comRecommend this page to a friend: |

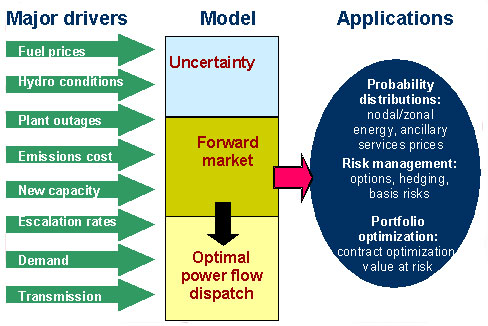

Price forecastingby Anne Ku (May 2002) original draft of article published in May/June 2002 issue of Platts Energy Business and Technology [deck] Electricity price forecasting has evolved from forecasting fuel costs to modelling electricity markets. It has become increasingly necessary and more complex for all kinds of market participants, as evident from the various approaches that exist today.[main text] Under regulated regimes, all price forecasting was cost forecasting, or forecasting the components that make up the price. In competitive markets, prices are less predictable and forecasting prices involves understanding the uncertainties surrounding the drivers of price as well as results of forecasting models. Unlike load forecasting models ("The art of forecasting demand" GEB Mar/April 2002, page 20) which can be developed and maintained in-house, price forecasting is far more complex. Who needs price forecasts?Developers, generators, investors, traders, and load serving entities need to know future electricity prices as their profitability depends on them. Credit rating agencies need to monitor the exposure of different players in the market to price fluctuations and risks. Load serving entities need to know how much power their customers are likely to use and how best to secure their needs through a mix of long term and short term contracts. Transmission organizations need to know how price variations among different regions may affect dispatching of generators and demand on the transmission networks. Large industrial customers need to assess their exposure to market price volatility and hedge their risks through long-term, fixed price contracts, participation in demand response programs, time of use rates, interruptible load programs and so on. For investors, lenders, and developers, it is critical to have the numbers. Dr Fereidoon P. Sioshansi, global manager of Power Market Advisory Products at Sacramento-based Henwood Energy Services believes that an educated forecast based on fundamentals of supply and demand is better than no forecast at all. In project finance, price forecasts are used extensively as the basis for input into development and acquisition investment and lending pro formas (spreadsheets that model the performance of an investment over time). Daniel E. White, executive vice president, Pace Global Energy Services, Fairfax, Va, explains that pro formas all rely on forward assumptions as to costs and revenues. Where there is market volatility and uncertainty, more detailed attention is paid to the support for the assumptions, and the assumptions themselves become more complicated. For example, in US markets with volatile fuel and power prices, pro formas for power plant financing are employing increasingly more complex forecasts of how fuel and power markets behave in an effort to more accurately model the power plants expected performance. Pace Global uses a range of quantitative and qualitative tools to develop their views, such as deploying different forecasting models for short, medium, and long term. Which approach?While many independent third-party commercial models exist today, there are basically two very different approaches in getting future prices. The pure forecast approach takes prices generated from models. The forward curve approach infers prices from observable trades in the market. In immature markets like electricity, it is easy to confuse "forward curves" with "price forecasts" (see box). In general, forward curves are made up of forward prices which reflect what people are will to pay today for delivery in the future. Implicit is the assumption of transactability, liquidity, and willingness to transact. When we speak of price forecasts, we are interested in price levels in the future, usually spot price: how much we will pay and receive the commodity at that point in the future when the power is generated. This is spot price forecasting. Pankaj Sahay, director of PricewaterhouseCooper's Energy Risk Measurement Group elaborates on these two approaches. In illiquid markets or where no markets exist such as that for long term electricity sales, it makes sense to use the fundamentals approach of looking at drivers of supply and demand, that is, the physical reality of plants on the ground, transmission assets, etc. In the short term or where markets do exist, you can take prices from what's being traded in the market. These prices are what make up the forward curve, which Sahay considers to be the single most important factor in financial valuations. The main difference between the two is whether you take prices that come out of a model or those that come from observable trades. Dr Aram Sogomonian, VP risk management, Constellation Energy Group, Baltimore, Maryland, observes that most energy companies use a variety of tools, history, extended market quotes, production models, heat rate models, and replacement cost models (how much does it cost to build a new plant). A trader-centric company would lean towards using heat rate models and market quotes, while the more traditional utilities would consider the long term fundamentals, such as those driven by plants that come on line or retire. The choice of approach also depends on the accounting treatment, for example, utilities tend to use accrual based accounting. Shorter term forecasts tend to rely more on the market rather than models. He adds that auditors have an important part to play in ensuring consistency because forecasts can be biased. Many forecasters have tried using time-series analysis to forecast electricity prices and their volatility. But this isn't always successful, claims Dr Pushkar Wagle, senior economist at LCG Consulting, Los Altos, Ca.. To avoid the pitfalls of an historical analysis, he says, you must recognize that electricity prices are strongly related to fundamental physical drivers, such as loads, hydrological conditions, fuel prices, unit operating characteristics, emission allowances, and transmission capability (figure 1). Moreover, to arrive at consistent forecasts across a range of products, the interaction between the various commodity, temporal, and location markets must be captured. In addition to market protocols, regional and system-wide reliability policies influence the operation and exchange of energy. The energy, ancillary service and allowance markets interact with each other, thereby affecting the bidding behavior of participants. Wagle advises that any modeling approach should be able to deal with a multi-commodity setting (allowing opportunity for electric generators to arbitrage among energy, ancillary service and capacity reserve commodities), and a multi-market setting (an opportunity for participating in different geographic locations and time periods). The model should provide a consistent set of energy, ancillary service, and capacity reserve prices in forward markets and real time markets, in the context of the market design and protocols. Seasoned forecasters and strategists note that most models fall somewhere in between the two approaches. According to Dr. Andy Van Horn, managing director and principal at Van Horn Consulting Group, Orinda, Calif., the engineering-based approach of power flow models and production cost simulation relies on how systems have operated in the past, incorporating data such as electrical properties of units and transmission grids. Econometric models which are essential for load forecasting predict how consumers will behave by examining historical relationships and extrapolating them forward. But the presence of ancillary service markets, markets with different rules and protocols, new power plants coming on-line, and changes in fuel prices make it difficult for econometric models by themselves to be used in price forecasting. The more sophisticated models combine market economics, such as bidding behavior that reflects opportunity costs, and system fundamentals. The art of price forecasting, he says, involves capturing the big picture as well as getting the details right. He adds that analyzing uncertainties in key market drivers is critical for making informed decisions. Uncertainty in price forecastsIn the early days of deregulation, many people thought that price forecasting would make them a lot of money. The reality is that forecasts are uncertain because a lot of price determinants are not known in advance, such as weather, which affects demand, and future rainfall, which affects the availability and amount of hydro generation. Dr Vic Niemeyer, area manager for Retail and Power Markets research at EPRI, helps utilities estimate prices as well as the volatility of prices. In his experience, a lot of the uncertainty won't resolve until the last day. Knowing how much uncertainty and the likelihood of high or low prices can be valuable. So expectations of price need to have measures of uncertainty attached to them. One way around understanding the uncertainty is to ensure consistency in the way forecasts are developed and used. Dallas-based TXU take a long term fundamentals based approach so as not be influenced by market emotions. They rely on their own forecasting, though mindful of what is forecasted elsewhere. For very large projects, they will look at independent forecasts in addition to internal forecasts. In the short term, when there is market guidance and liquidity, they take approach that market is right. TXU's VP of analysis and structuring Manu Asthana says "there is more uncertainty in price forecasting than load forecasting, and it's more complex because we're forecasting both supply and demand. It requires additional sets of skills, particularly more of engineering background. We take great care to incorporate forecasting uncertainty into the application of forecasts." TXU runs its business as one global enterprise with the same risk management philosophy and discipline across its operations. As such, it has a process for rigorous independent validation of price forecasts. Every forecast is independently validated by a global middle office team, which is led by a global chief risk officer. Another way to understand the uncertainty is to look at different scenarios, advises Van Horn. But most people tend to focus uncertainty analysis around business as usual rather than unlikely situations. It's also important to carry out sensitivity analysis, to see which and how variables affect prices. Concerning the way people use price forecasts, real options analysis tries to account for flexibility that people have in updating decisions in the future. Van Horn adds that new legislation, such as environmental controls and pollution regulation, is often left out in forecasting models as they are difficult to anticipate and analyze. The important thing, Van Horn says, is to understand the strengths and limitations of models as this will aid your own intuition about markets. Are you using the right models for the right purpose? According to Eric Toolson, senior vice president at Henwood Energy Services, understanding the drivers in the market is more important than the forecast itself. In-house or outsource?Most utilities do a combination of purchasing independent commercial models as well as using in-house models, which are typically sophisticated spreadsheets or databases, says Joanna Cloud, principal consultant at Atlanta-based New Energy Associates. Users may even ask industry consultants to run models, that is, produce forecasts rather than maintaining the models themselves. The sheer amount of effort required for data maintenance and model support often makes this a better strategy than allocating dedicated resources in-house. Independent commercial models have taken a long time to develop and are continuously refined. "You not only get quality control, embedded capability from years and years of refinement, but also impartiality. In-house models often die when the key developer leaves," says Greg Turk, president, M.S. Gerber and Associates, Columbus, Ohio. "However, the commercial models provide institutional stability." Running and maintaining a detailed production cost model and a faster one to do a multi-area model is a full-time job. If they also develop their own database, they will get killed over time. According to Don Winslow, vice president of mid office for Portland (Ore.)-based PacifiCorp Power Marketing, a non-regulated subsidiary of Scottish Power, their in-house price forecasters work closely with their risk management group which validates their assumptions. "We use a combination of a leased vendor model, consultants' forecasts and our own spreadsheets which incorporate forward prices for natural gas and power. The primary motivation for using the models is to understand the market drivers and the relationship of regional prices (as opposed to determining an absolute estimate of the price levels). The single biggest driver for the model outputs is the price of natural gas, which is an exogenous input to the model. Thus, our estimates of the level of long term power prices are only as good as our estimates of long term gas prices." Dr Tony Ligeralde, General Manager of Research & Analytics, Cinergy Corp, Cincinnati, Ohio has been looking at price forecasting for a number of years. His group originally hired consultants to build their proprietary models, but have since transferred the maintenance and modifications in-house. However, they continue to compare their own forecasts with third party forecasts to get an understanding of what others are thinking. He warns against relying solely on a pure price forecast because the output might be nowhere close to where the market trades. The question then arises "is the model wrong or is the market not accounting for all the information?" This is especially important when valuing longer-dated deals where the market is less liquid. For purposes of marking such transactions to market, calibrating the model to visible market indications helps ensure consistency between the visible and the model generated curve. Ligeralde anticipates that new disclosure requirements by rating agencies after the Enron collapse will accelerate the development of an industry standard for modelling the non-liquid portion of the price curve. He says, "When deals are being marked to model, you have to worry about model risk." Less data, more uncertaintyPrice forecasting models are data-intensive. Henwood's price forecasting model MarketSym, for instance, takes data from 500 different sources. With further deregulation and competition, companies will have less incentive to report and share information. Gone are the days of free public data pulled from FERC forms. "The emphasis of price forecasting will shift away from data points to uncertainty around the data," says New Energy Associate's Cloud. The collection of specialist data is already becoming a niche industry. Such data experts will become increasingly valuable as the sophistication of price forecasting models reach steady state. |

Box: Forward curve vs price forecast Figure 1 Fundamental drivers of price and

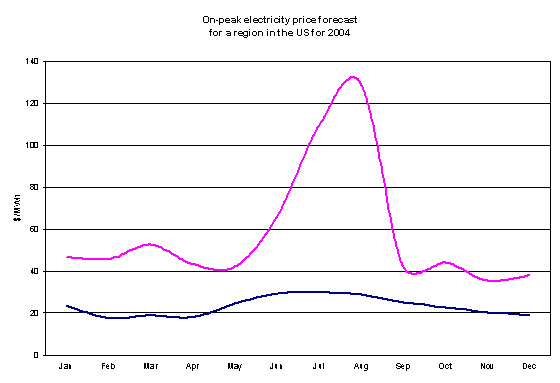

how they feed into model approach and results Figure 2 Electricity prices are very volatile,

as seen in the range of forecast prices Visit these sites for more information: Independent commercial price forecast model vendors/consultants: Others mentioned in article: |

||

{kind=link}

{kind=link}